East Bay April '24 Real Estate Update Ascend RE

Ascend RE April 18, 2024

Alameda

Ascend RE April 18, 2024

Alameda

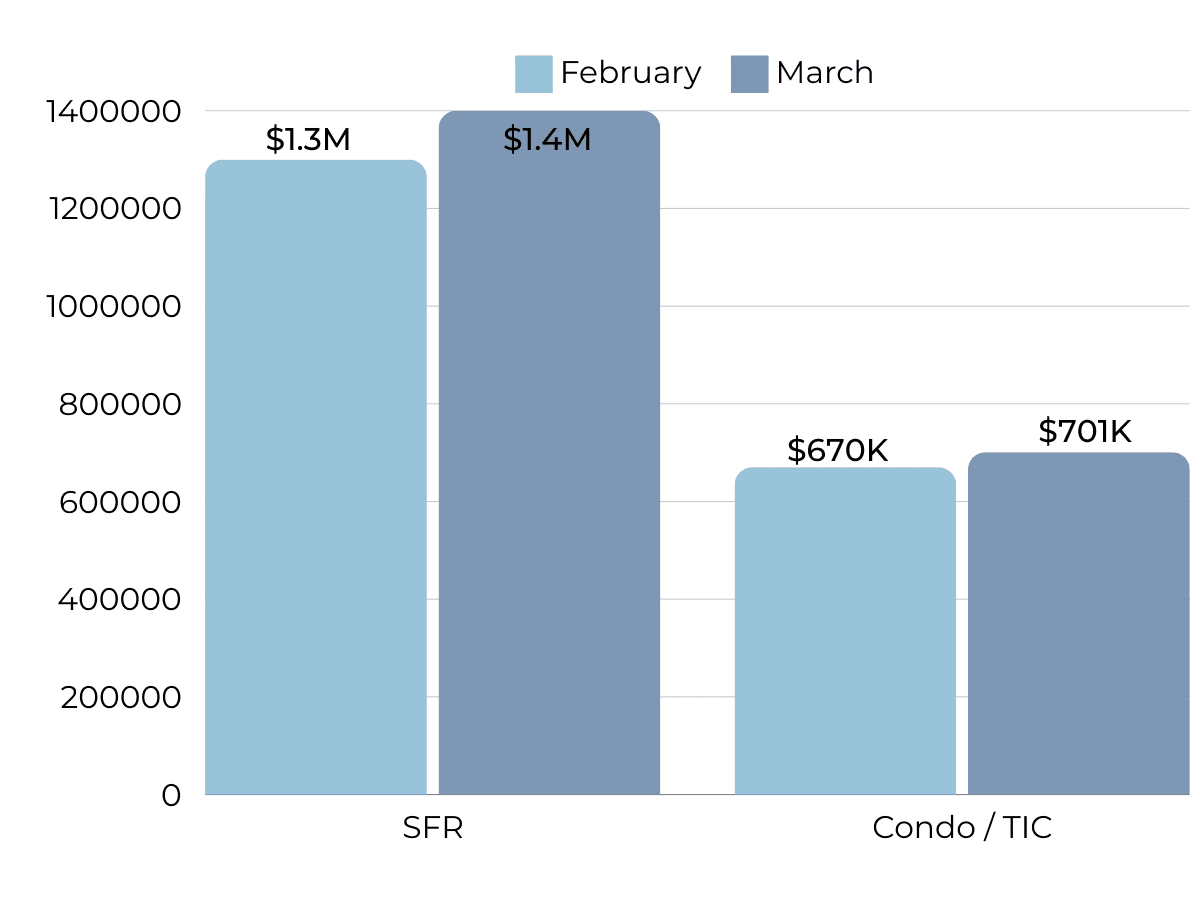

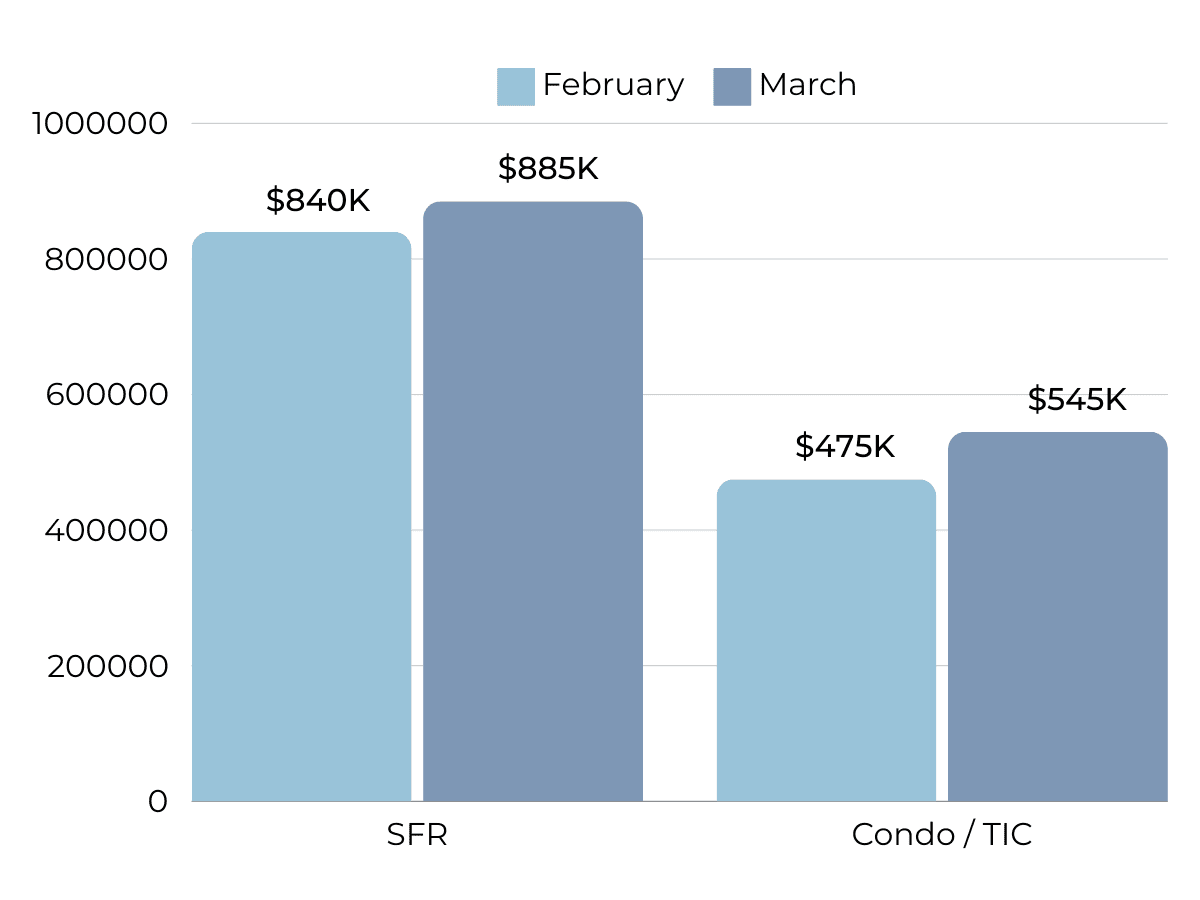

In the East Bay, low inventory and high demand have more than offset the downward price pressure from higher mortgage rates, and prices generally haven’t experienced larger drops due to higher mortgage rates. Month over month, in February, the median single-family home price rose 18% in Alameda and 10% in Contra Costa. Year over year, prices were up 22% in Alameda and 13% in Contra Costa. Condo prices were up month over month and year over year in Alameda, though they dropped in Contra Costa. We expect prices in the East Bay to remain slightly below peak until late spring, but as interest rates decline, prices will almost certainly reach new highs in the first half of 2024. Additionally, inventory is so low that rising supply will only increase prices as buyers are better able to find the best match.

High mortgage rates soften both supply and demand, but at this point rates have been above 6% for 15 months, and rate cuts will likely occur sometime this year. Potential buyers have had longer to save for a down payment and will have the opportunity to refinance in the next 12-24 months, which makes current rates less of a limiting factor. However, high demand can only do so much for the market if there isn’t supply to meet it.

In 2023, inventory didn’t have anything resembling the typical sine wave, since far fewer sellers came to the market, especially in the first half of the year, and the low inventory and fewer new listings slowed the market considerably. New listings have been exceptionally low, so the little inventory growth last year was driven by softening demand. Typically, inventory peaks in July or August and declines through December or January. However, in 2023, inventory peaked in October, further highlighting the atypical supply trend. In November and December, inventory, sales, and new listings dropped, reaching all-time low inventory in December 2023.

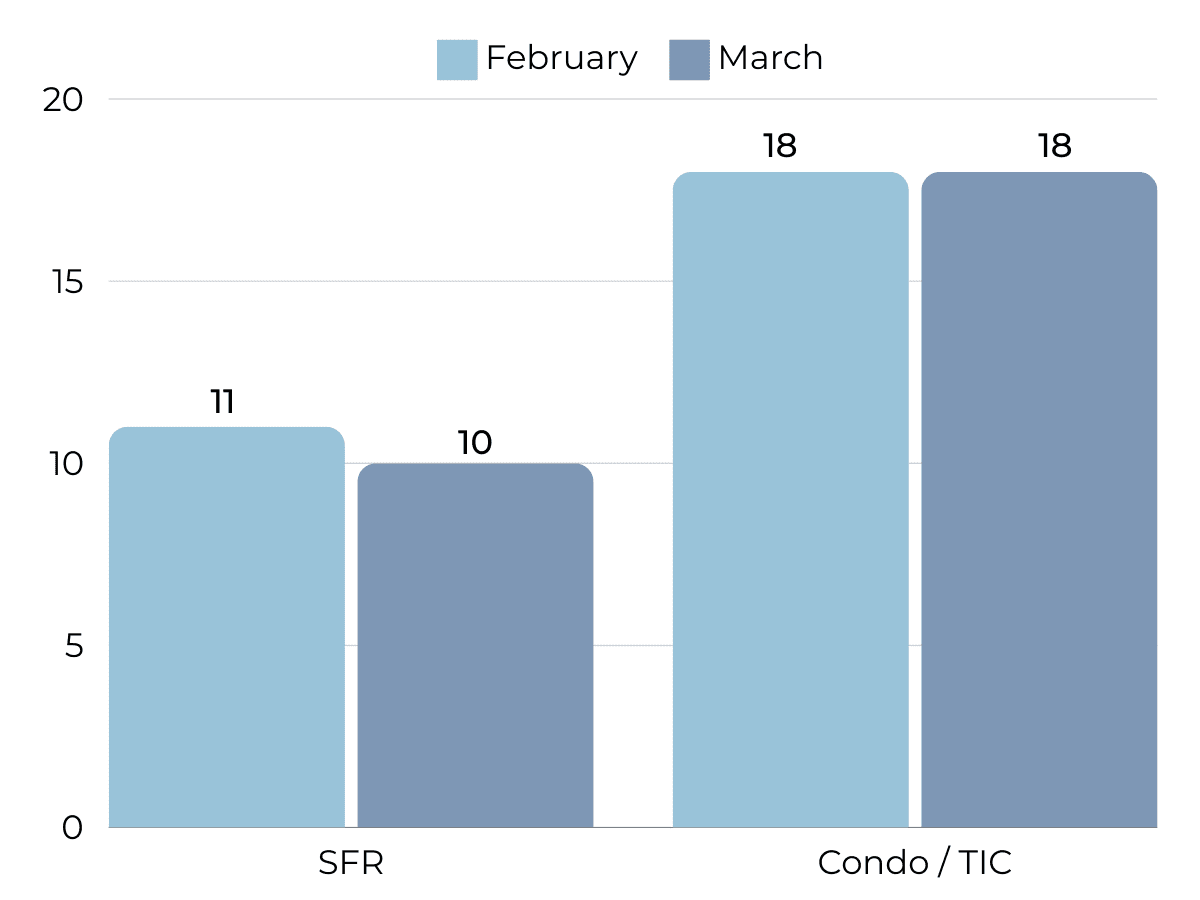

In January and February 2024, single-family home and condo inventory and new listings increased. With the current low inventory levels, the number of new listings coming to market is a significant predictor of sales. New listings increased 7% month over month, and sales increased 30%. Year over year, inventory is the same as last February; however, sales and new listings are up 10% and 16%, respectively. The next three months will be critical to our understanding of the market. More supply will mean a healthier market and a more normal housing market in 2024.

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). The East Bay market tends to favor sellers, which is reflected in its low MSI. MSI fell sharply in the first quarter of 2023 before gently trending higher from May to November. In December, MSI declined sharply, but rose again in January. MSI contracted once again in February and currently indicates a sellers’ market for both single-family homes and condos.

We can also use percent of list price received as another indicator for supply and demand. Typically, in a calendar year, sellers receive the lowest percentage of list price during the winter months, when demand is lowest. Winter months tend to have the lowest average sale price (SP) to list price (LP), and the summer months tend to have the highest SP/LP. The January and February 2024 SP/LP were both 4% higher than last year, meaning we expect sellers overall to receive a higher percentage of the list price throughout all of 2024 than they did in 2023.

1. Price Stability: Overall, housing prices in both Contra Costa and Alameda County remained relatively stable compared to previous months. While there were fluctuations in specific neighborhoods and property types, the market as a whole showed a consistent trajectory with modest appreciation.

2. Limited Inventory: Inventory levels continued to be tight across both counties, with a shortage of available homes for sale. This scarcity of inventory put upward pressure on prices and led to competitive bidding situations, making it challenging for prospective buyers to find suitable properties.

3. Strong Demand: Demand for housing remained robust in Contra Costa and Alameda County, driven by factors such as employment opportunities, desirable locations, good schools, and transportation infrastructure. This sustained demand contributed to quick sales and multiple offers in many instances.

4. Affordability Challenges: Affordability remained a significant concern for many residents, particularly first-time buyers and middle-income earners. High housing costs relative to income levels continued to pose barriers to homeownership and rental affordability, prompting some buyers to explore alternative areas or housing types.

5. Suburban and Urban Dynamics: Suburban areas in both counties continued to attract interest from buyers seeking more space, quieter neighborhoods, and better affordability compared to urban cores. However, urban areas with access to amenities, public transportation, and employment centers remained popular among certain demographics, contributing to varied dynamics across different neighborhoods.

6. Rental Market: The rental market in Contra Costa and Alameda County experienced mixed trends, with some areas witnessing stable rents while others saw slight fluctuations. Factors such as employment trends, remote work preferences, and lifestyle shifts influenced rental demand and pricing dynamics.

7. Investor Activity: Real estate investors continued to show interest in both counties, targeting properties with potential for appreciation and rental income. However, cautious optimism prevailed amid economic uncertainties and regulatory changes, leading investors to carefully assess opportunities in the market.

Overall, the housing markets in Contra Costa and Alameda County in February 2024 demonstrated resilience and attractiveness to buyers and investors, despite challenges such as limited inventory and affordability concerns. Strong demand, desirable locations, and varied housing options contributed to the stability and moderate growth observed in these markets.

Recent

Browse our blog posts to be in the know.

Provided Courtesy of Ascend Real Estate

Provided Courtesy of Ascend Real Estate

Provided courtesy of Ascend Real Estate

Welcome to our September newsletter, where we’ll discuss residential real estate trends in the East Bay and across the nation. This month, we’ll examine the state of t… Read more

The Big Story What to expect when you’re expecting inflation Quick Take: The number of homes sold in 2021 is set to be one of the highest on record. Inflation reached … Read more

Welcome to our September newsletter, where we’ll discuss residential real estate trends in Silicon Valley and across the nation. This month, we’ll examine the state of… Read more

Welcome to our September newsletter, where we’ll discuss residential real estate trends in San Francisco and across the nation. This month, we’ll examine the state of … Read more

As we end another crazy year, we are very grateful our kids are finally fully vaccinated, and a return to some sense of normalcy is in view. We are especially looking … Read more

Summer is here, and so are the boozy slushies, all-you-can-eat tacos and double cheeseburgers

The Big Story Where can home prices go from here? Quick Take: Home prices appreciated faster in 2021 than at any other time, even surpassing the 2004–2006 housing bubb… Read more

No doubt 2021 Bay Area housing markets was one of the wildest in recent memory! Our local real estate experts will share their year-end analysis of San Francisco, East… Read more

Welcome, welcome, welcome to 2022. Low inventory here in San Francisco gave us Realtors® a short respite. I took advantage of the slowdown and spent some time tailgati… Read more

Happy Autumn! With all the harvest festivals, this is one of my favorite times of year. My kids love the pick-your-own pumpkin activities, and we look forward to our a… Read more

Welcome to our October newsletter, where we’ll explore residential real estate trends in the East Bay and across the nation. This month, we examine the state of the U.… Read more

You’ve got questions and we can’t wait to answer them.