San Francisco May Market Update

Manuel Solis May 17, 2021

Real Estate

Manuel Solis May 17, 2021

Real Estate

Welcome to our May newsletter, where we dive into national and local residential real estate trends. This month, we examine how the housing undersupply is increasing home prices and paving the way toward a more balanced market. We also discuss the sharp decrease in mortgage rates and the state of employment, which is historically one of the leading indicators of home valuations.

Currently, the housing supply is so low that demand far outpaces the number of homes on the market. Freddie Mac estimates that the United States is about 4 million homes short of meeting buyer demand. The housing shortage compounds when potential home sellers decide to stay out of the market because they feel they won’t be able to find a home to buy after they sell. Home builders, who have been slow to ramp up production after the 2008 crash, are drastically increasing new construction because they want to capitalize on the sustained demand for housing.

We expect relative housing demand to remain high over the next 12 months at the very least. New homes take time to build and will not come to market at the rate necessary to balance it. In March 2021, U.S. home builders started constructing homes at a seasonally adjusted annual rate of 1.74 million, up 37% compared to March 2020. New construction will eventually alleviate some of the shortage, but housing will remain undersupplied for months, if not years, to come.

As we navigate this period of high buyer demand and low supply, we remain committed to providing you with the most current market information so you feel supported and informed in your buying and selling decisions.

In this month’s newsletter, we cover the following:

Key Topics and Trends in May

Last year, many individuals and families experienced feast or famine. Those lucky enough to stay financially unaffected by the pandemic were likely saving or investing more than expected, accruing more and more capital. At the same time, interest rates plummeted to hyperlow levels as millennials, the largest living adult generation, grew to prime homeownership age. With these factors combined, we saw the demand for homes skyrocket in 2020. The near-universal ability to work remotely changed motivations for moving. Relocating for a job or to be closer to the office was no longer necessary. However, due to the unique requirements of working from home, people began wanting more space. As a result, single-family home demand rose steeply, while condo demand lagged. As sellers listed condos, they bought single-family homes, driving single-family home inventory down. As the supply of homes declined, fewer new listings came to market—in part, because of the difficulty of finding a new home after selling.

One reason for the housing shortage has been the understandable hesitancy of builders to construct new properties since the 2006–2008 housing crash; however, this lack of new construction means that there aren’t enough homes on the market to meet the unexpectedly high demand. Over the last six months, new construction has ramped up considerably to an annualized 1.74 million new homes. The largest gains in new-home construction occurred in the Midwest, where housing starts more than doubled on a monthly basis. The Northeast and the South also saw faster rates of new-home construction, while home-building activity slowed in the West. Additionally, established metro areas lack land upon which to build, so adding meaningfully to supply through new construction can be challenging or fully unattainable.

As you can see from the chart below, new construction is now in the pre-housing bubble levels as home builders react to the surge in home prices and demand.

Mortgage rates rose significantly, slightly over 50 basis points, from January 2021 to mid-April 2021, but dropped sharply back below 3% in the second half of April. Although interest rates are still expected to rise to 3.7% over the course of the year, according to the Mortgage Bankers Association, the mortgage rate drop shows the non-linear path that rates will likely take. Because the mortgage rate affects affordability, the current low rate will only increase demand in the short term.

High unemployment is one of the strongest predictors of falling home prices over a two-year period. The chart below illustrates the employment cost of a recession. Total employment tends to grow at a fairly consistent rate during economic expansions. The green line illustrates the expected level of employment had the pandemic never happened. As that green line shows, we are nearly 11 million jobs below where employment was expected to be after the first quarter of 2021. Twice as many workers are currently unemployed than in February 2020. The initial pain of unemployment has been dampened by government relief. Mortgages in forbearance and foreclosures are low, as are delinquencies in credit card debt. However, we will continue to monitor unemployment in order to gauge future market conditions.

Although we don’t expect the same level of buying in 2021 that we saw in 2020, the environment is right for demand to outpace supply in 2021. In the short term, we may even see a demand spike as potential buyers try to purchase before rates rise higher. As a result, we anticipate a competitive landscape for buyers over the course of this year.

While the market remains competitive for buyers, conditions are making it an exceptional time for homeowners to sell. Low inventory means multiple offers and fewer concessions. Because sellers are often selling one home and buying another, it is essential that sellers work with the right agent to ensure the transition goes smoothly.

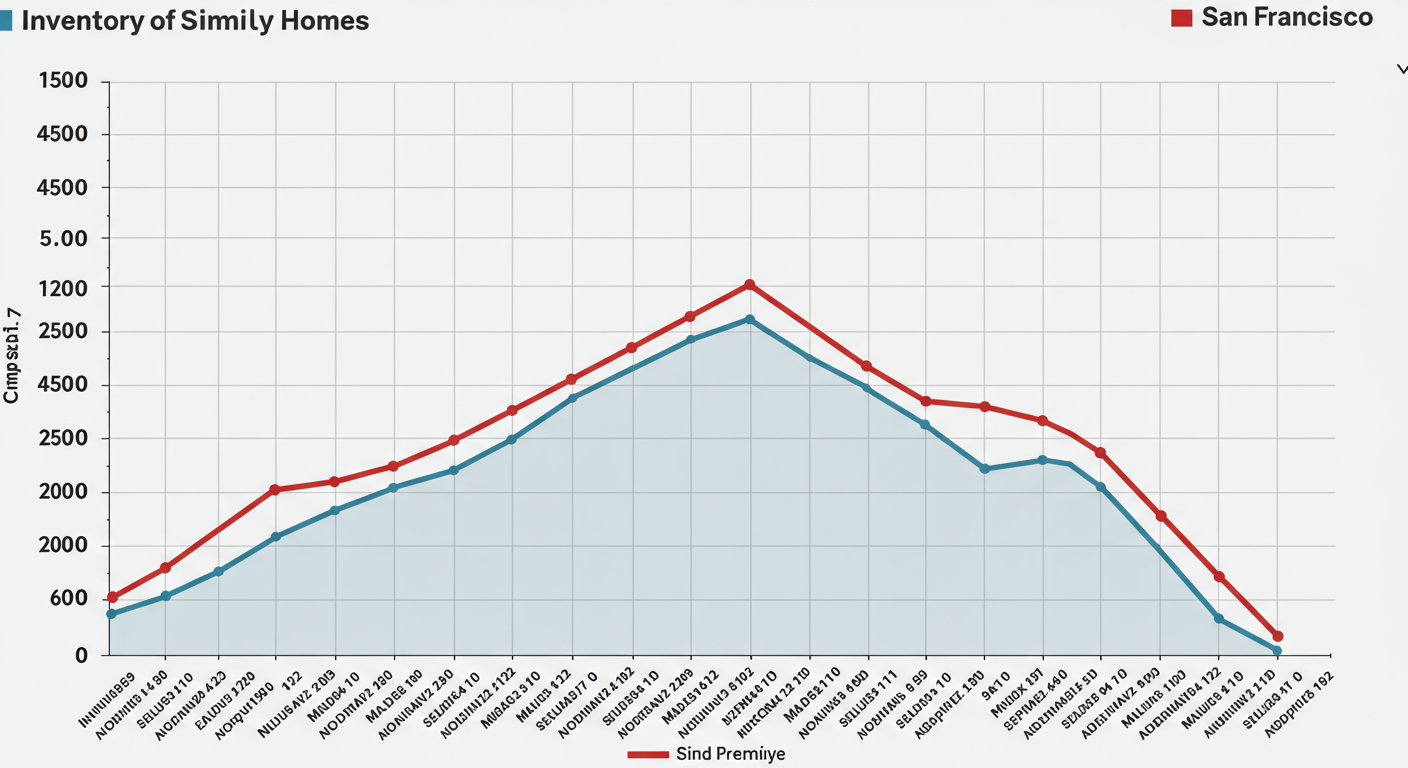

May Housing Market Updates for San Francisco

During April 2021 in San Francisco, the median single-family home price rose once again to an all-time high, and condo prices fell. Year-over-year, single-family home prices meaningfully increased, up 10%, while condo prices declined 5%.

In 2020, single-family home inventory increased to its highest level since 2011. From May to September 2020 (five months), inventory exploded. But we need to look at it through the lens of a city in a constant state of single-family home undersupply. Despite such a meteoric rise, inventory fell even faster than it rose, which speaks to the desirability of San Francisco. By January 2021, inventory declined to lower levels than January 2020, then ticked up slightly in February and March before going lower still in April 2021. As you can see from the chart, sales outpaced new listings in March and April. With such a consistently high level of demand, prices will likely continue to appreciate throughout 2021.

The number of condos on the market fell in April but remains higher than last year. Demand for condos has come back strong, and sales outpaced new listings in March and April. Sales in April 2021 significantly outpaced sales in both April 2020 and 2019.

Both single-family homes and condos spent less time on the market in April 2021 than they did last year. As we will see, the pace of sales has contributed to the low Months of Supply Inventory (MSI) over the past several months.

We can use MSI as a metric to judge whether the market favors buyers or sellers. The average MSI is three months in California (far lower than the national average of six months), which indicates a balanced market. An MSI lower than three means that there are more buyers than sellers on the market (that is, it is a sellers’ market), while a higher MSI means there are more sellers than buyers (that is, it is a buyers’ market). In April 2021, the MSI fell below one month of supply for single-family homes and below two for condos, indicating that the market favors sellers.

In summary, the high demand and low supply present in San Francisco have driven home price appreciation. Inventory will likely remain low this year with fewer sellers coming to market, potentially lifting prices higher. Overall, the housing market has shown its resilience through the pandemic and remains one of the most valuable asset classes. The data show that housing has remained consistently strong throughout this period.

We anticipate new listings to accelerate into the summer months. The current market conditions could withstand a high number of new listings coming to market, and more sellers could enter the market to capitalize on the high buyer demand. As we enter the spring season, we expect the high demand to continue, and new houses on the market to be sold quickly.

As always, we remain committed to helping our clients achieve their current and future real estate goals. Our team of experienced professionals are happy to discuss the information we’ve shared in this newsletter. We welcome you to contact us with any questions about the current market or to request an evaluation of your home or condo.

Recent

Browse our blog posts to be in the know.

Provided Courtesy of Ascend Real Estate

Provided Courtesy of Ascend Real Estate

Provided courtesy of Ascend Real Estate

Welcome to our September newsletter, where we’ll discuss residential real estate trends in the East Bay and across the nation. This month, we’ll examine the state of t… Read more

The Big Story What to expect when you’re expecting inflation Quick Take: The number of homes sold in 2021 is set to be one of the highest on record. Inflation reached … Read more

Welcome to our September newsletter, where we’ll discuss residential real estate trends in Silicon Valley and across the nation. This month, we’ll examine the state of… Read more

Welcome to our September newsletter, where we’ll discuss residential real estate trends in San Francisco and across the nation. This month, we’ll examine the state of … Read more

As we end another crazy year, we are very grateful our kids are finally fully vaccinated, and a return to some sense of normalcy is in view. We are especially looking … Read more

Summer is here, and so are the boozy slushies, all-you-can-eat tacos and double cheeseburgers

The Big Story Where can home prices go from here? Quick Take: Home prices appreciated faster in 2021 than at any other time, even surpassing the 2004–2006 housing bubb… Read more

No doubt 2021 Bay Area housing markets was one of the wildest in recent memory! Our local real estate experts will share their year-end analysis of San Francisco, East… Read more

Welcome, welcome, welcome to 2022. Low inventory here in San Francisco gave us Realtors® a short respite. I took advantage of the slowdown and spent some time tailgati… Read more

You’ve got questions and we can’t wait to answer them.